Date: March 12, 2026

The Lead: A World on Edge

Global financial markets are navigating a high-stakes "tug-of-war" today as the escalating conflict in the Middle East collides with fresh economic data. While U.S. inflation figures for February showed a "tame" headline of 2.4%, the market's gaze has shifted toward the Strait of Hormuz. With the waterway effectively blockaded by Iranian naval activity, energy prices have surged, threatening a new wave of "imported inflation" that could derail central bank plans for interest rate cuts.

1. Commodities: Gold and the "Oil Shock"

Gold remains the primary focus for safety-conscious investors. Despite a slight pullback due to a resurgent U.S. Dollar, the metal is holding firmly above the $5,150 mark.

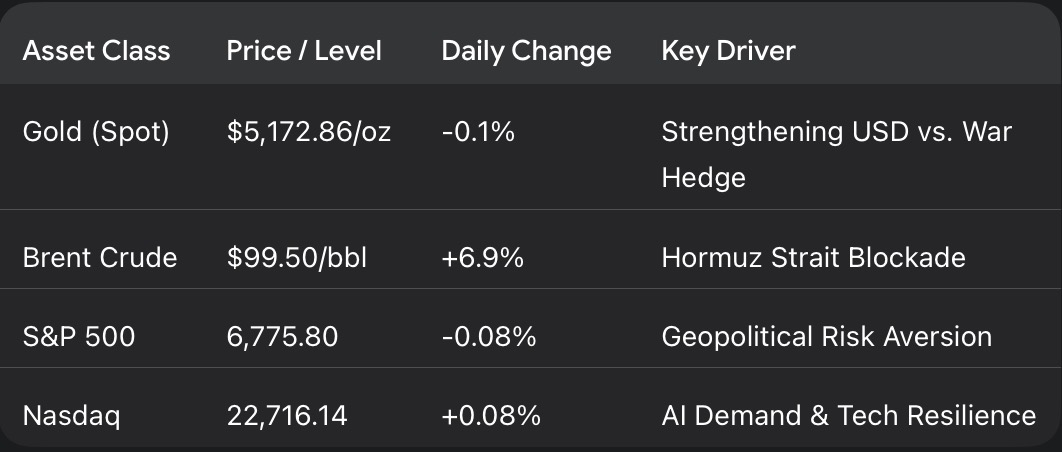

• Gold Status: Spot gold settled near $5,172 per ounce. Analysts at ABC Refinery note that "any dips are being bought," as the market lacks a structural reason to sell while the threat of a wider regional war persists.

• The $200 Threat: Crude oil futures jumped nearly 5% after Iran warned the world to brace for $200-per-barrel oil.

• Emergency Measures: The International Energy Agency (IEA) has authorized a record release of 400 million barrels from strategic reserves to blunt the shock, though markets remain skeptical that this can offset the 15-million-barrel daily shortfall from the Gulf.

2. Equities: Wall Street & The "PAYP" Debut

While the Dow and S&P 500 closed lower on Wednesday due to war jitters, the tech sector provided a glimmer of optimism.

• PayPay IPO: In a landmark event for the fintech sector, SoftBank’s PayPay Corporation priced its IPO at $16 per ADS. Trading begins today on the Nasdaq under the symbol "PAYP."

• Corporate Earnings: Oracle shares jumped over 9% following strong revenue guidance fueled by the 2026 AI spending boom. Conversely, Campbell’s tumbled 7.1% after cutting forecasts due to rising tariff pressures and supply chain disruptions.

3. Global Monetary Policy

The "Higher for Longer" narrative has gained new life as energy-driven inflation looms.

• The Fed: Investors have scaled back expectations for rate relief. The Federal Reserve is widely expected to hold rates at 3.50%–3.75% next week, with many now pricing in only one 25-basis-point cut for the entire year.

• The RBA (Australia): Australia’s "Big Four" banks are now in rare agreement, predicting the Reserve Bank of Australia will hike rates again next Tuesday to combat persistent domestic price pressures.

Market Summary Table

Looking Ahead

Looking Ahead

Investors are now looking to Friday's release of the Personal Consumption Expenditures (PCE) index, the Fed's preferred inflation gauge. This data will confirm whether the recent energy spike has already begun to bleed into broader consumer costs.